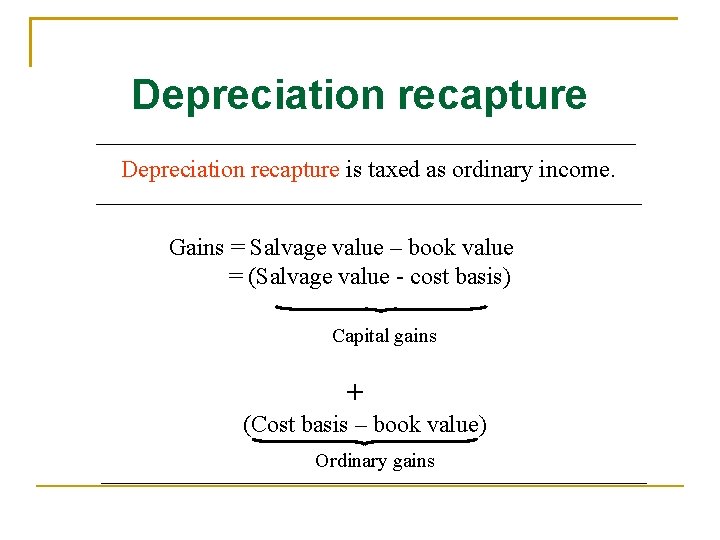

Depreciation recapture formula

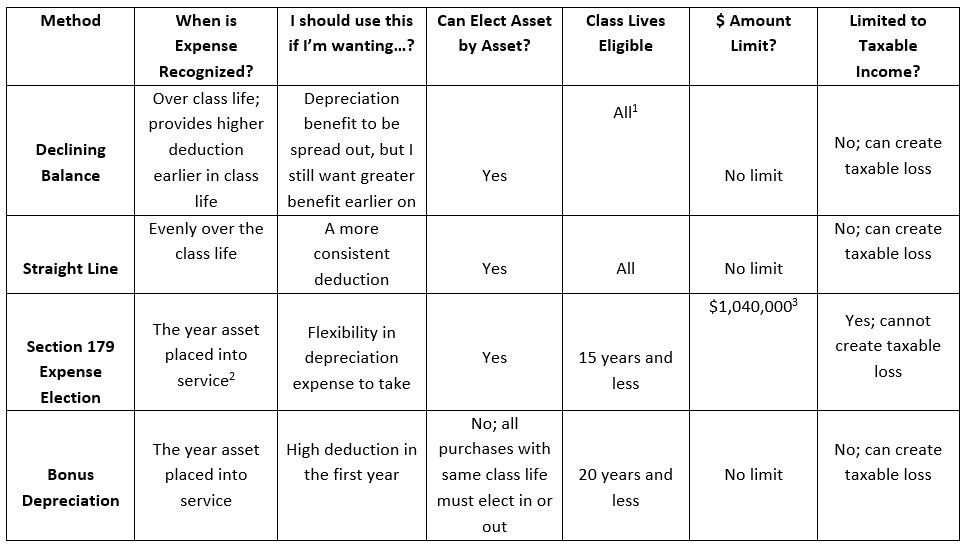

What Is Depreciation Recapture. The tax rate for the depreciation recapture will depend on whether an asset is a section 1245 or 1250 asset.

Learn About Depreciation Recapture Spartan Invest

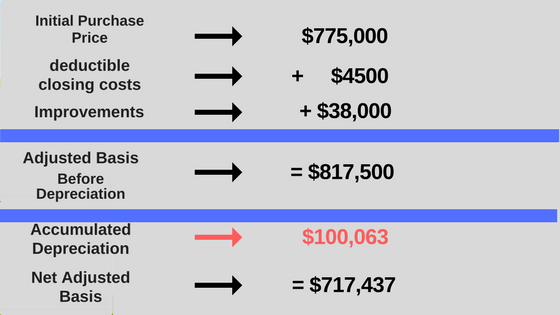

Heres the formula used to determine basis and depreciation on commercial assets.

. You can generally figure depreciation on the business use portion of your home up to the gross income limitation over a 39-year. Depreciation recapture tax rates Since depreciation recapture is taxed as ordinary income as opposed to capital gains your depreciation recapture tax rate is going to be your income tax rate with a cap at 25. A taxpayer whose average annual gross receipts is less than or equal to 10000000 may elect to not capitalize amounts paid for repairs maintenance or improvements of.

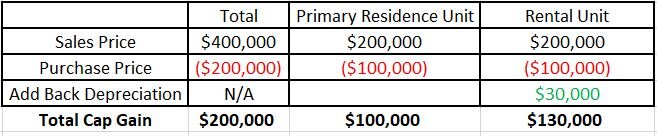

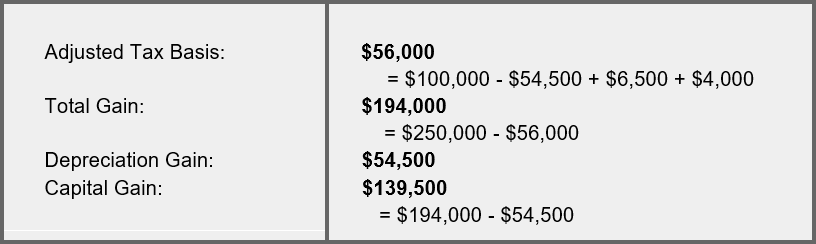

Or the capital cost of the property from his UCC and is left with a recapture of CCA of 4000 6000 - 10000 that he has to include in his business income. Capital assets might include rental properties equipment furniture or other assets. Recaptured Depreciation Formula The formula for calculation of recaptured deprecation is Recaptured depreciation Selling price of the asset Deprecated value of the asset where the depreciated value of assets is calculated as the original cost of the asset less deprecation on the value of assets over the years.

Schedule C Form 1040 Profit or Loss From Business Sole Proprietorship if youre a sole proprietor. You may also need to use Form 4562 Depreciation and Amortization. The taxpayer is liable to pay tax.

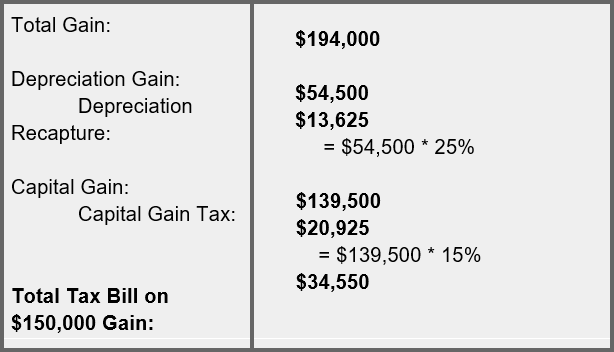

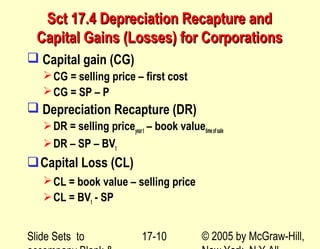

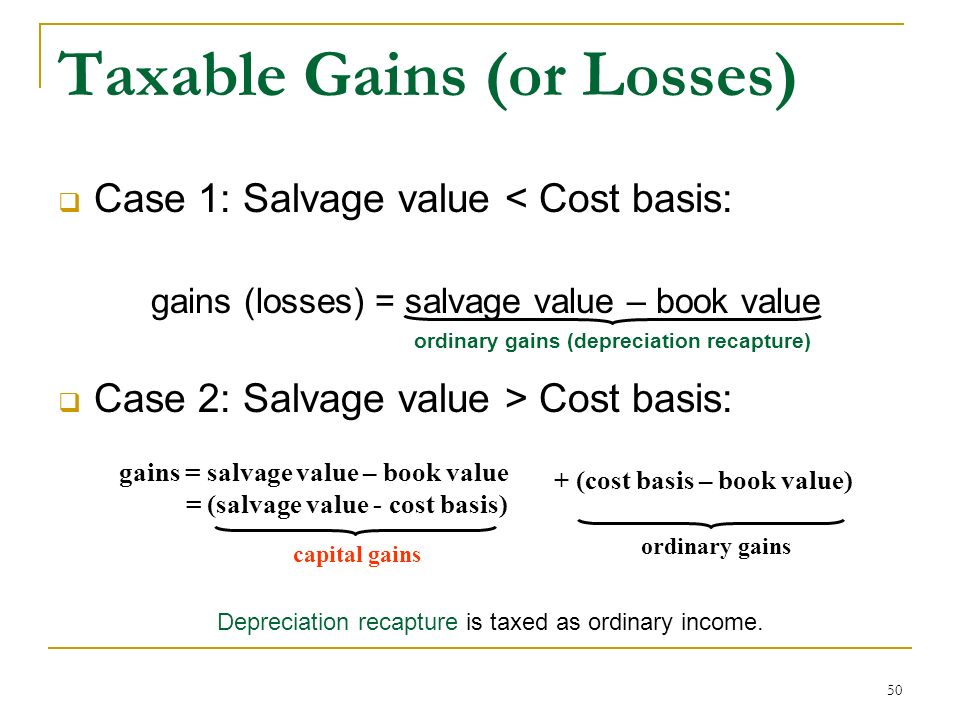

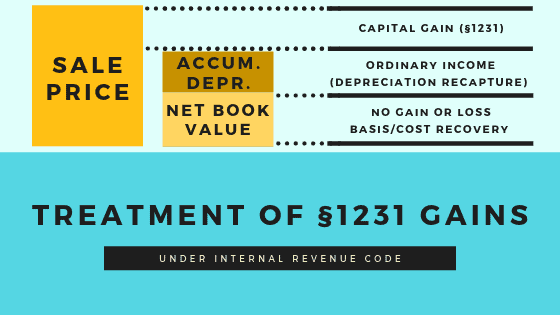

Your depreciation recapture tax rate will break down like thisShortcode. So between 218180 the accumulated depreciation over twenty years and 368180 the realized gain the depreciation recapture will be applied to 218180. Depreciation recapture is associated with the depreciable property and selling the depreciable property results in the ordinary income and reduces the capital gain reported for tax purposes.

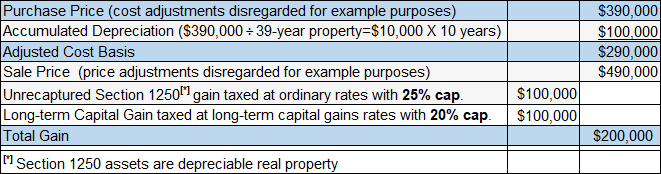

All allowed or allowable depreciation must be considered at the time of sale. QIP is 15-year property subject to the straight-line method of depreciation but is eligible for bonus depreciation under Sec. When an asset is sold at a value above the adjusted basis the gain is taxed as ordinary income up to the amount of depreciation claimed to the extent of the excess of accelerated depreciation that would have been allowed.

Depreciation recapture is a process that allows the IRS to collect taxes on the financial gain a taxpayer earns from the sale of an asset. He subtracts 10000 the lesser of the proceeds of disposition of the property minus the related outlays and expenses. One common depreciation recapture example involves qualified improvement property QIP.

You may be able to deduct the acquisition cost of a computer purchased for business use in several ways. This ordinary income treatment is referred to as depreciation recapture. Your calculation will look like this.

This 25 cap was instituted in 2013. Under Internal Revenue Code section 179 you can expense the acquisition cost of the computer if the computer is qualifying property under section 179 by electing to recover all or part of the cost up to a dollar limit by deducting. Previously the cap was 15.

QIP includes certain improvements to the interior portion of nonresidential real property Sec. But wait theres more. Cost of your property minus the value of the landBasis Basis divided by 139ththe amount you can depreciate annually How to Use a 1031 Exchange to Avoid.

For tax years beginning in 2022 the maximum section 179 expense deduction is 1080000. You can claim business use of an automobile on. If a farmer use Schedule F Form 1040 Profit or.

If you use this method you need to figure depreciation for the vehicle. This recapture income under IRC section 1245 or 1250 is also an example of hot assets. Section 1245 depreciation recapture is used to calculate any income tax or capital gains tax you may owe on a sold asset.

Need an Easy Accurate Way to Comply with State Depreciation Across Multiple States. This is a rare occurrence because the IRS has mandated all post-1986 real estate be depreciated using the straight-line method. Regular Method - No.

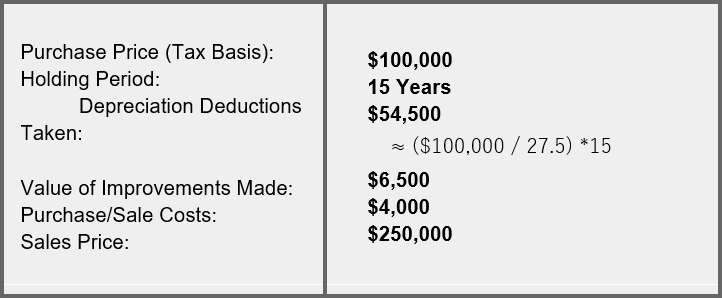

In this instance your capital gain on the property is 152560 102560 50000. 6 Multiply your capital gain by the capital gains tax rate and your depreciation recapture gain by your ordinary income tax rate to determine your total tax liability. Section 179 deduction dollar limits.

What is depreciation recapture. To calculate this you will start with the cost basis of the item then minus all depreciation on that item and finally add in your final sale price of the item. This limit is reduced by the amount by which the cost of section 179 property placed in service during the tax year exceeds 2700000Also the maximum section 179 expense deduction for sport utility vehicles placed in service in tax years beginning in 2022.

Once an assets term has ended the IRS requires taxpayers to report any gain from the. Examples of Depreciation Recapture. Your depreciation recapture gain is 102560.

Is generally depreciated over a recovery period of 275 years using the straight line method of depreciation and a mid-month convention as residential rental property. The tax rate will be tied to the investors tax brackethowever that rate cannot exceed 25 percent. Ad Expertly Manage the Largest Expenditure on the Balance Sheet with Efficiency Confidence.

In this situation the UCC is also 6000 10000 - 4000.

Rental Property Profit Calculator Watch Quick Video Mortgageblog Com

Chapter 8 Accounting For Depreciation And Income Taxes Ppt Video Online Download

1031 Exchange And Depreciation Recapture Explained A To Z Propertycashin

How To Use Rental Property Depreciation To Your Advantage

Depreciation Starting With The Basics Ilsoyadvisor

Learn About Depreciation Recapture Spartan Invest

Chapter 8 Depreciation And Income Taxes Ppt Video Online Download

Do I Have To Pay Tax When I Sell My House Greenbush Financial Group

Chapter 17 After Tax Economic Analysis

Contributed Property In The Hands Of A Partnership

Chapter 8 Accounting For Depreciation And Income Taxes Ppt Video Online Download

Solved A Property Purchased For 100 000 With An Noi Of 7 000 Per 10 Years Will Be Sold For 140 000 There Is No Cost Of Sale Depreciation Taken Course Hero

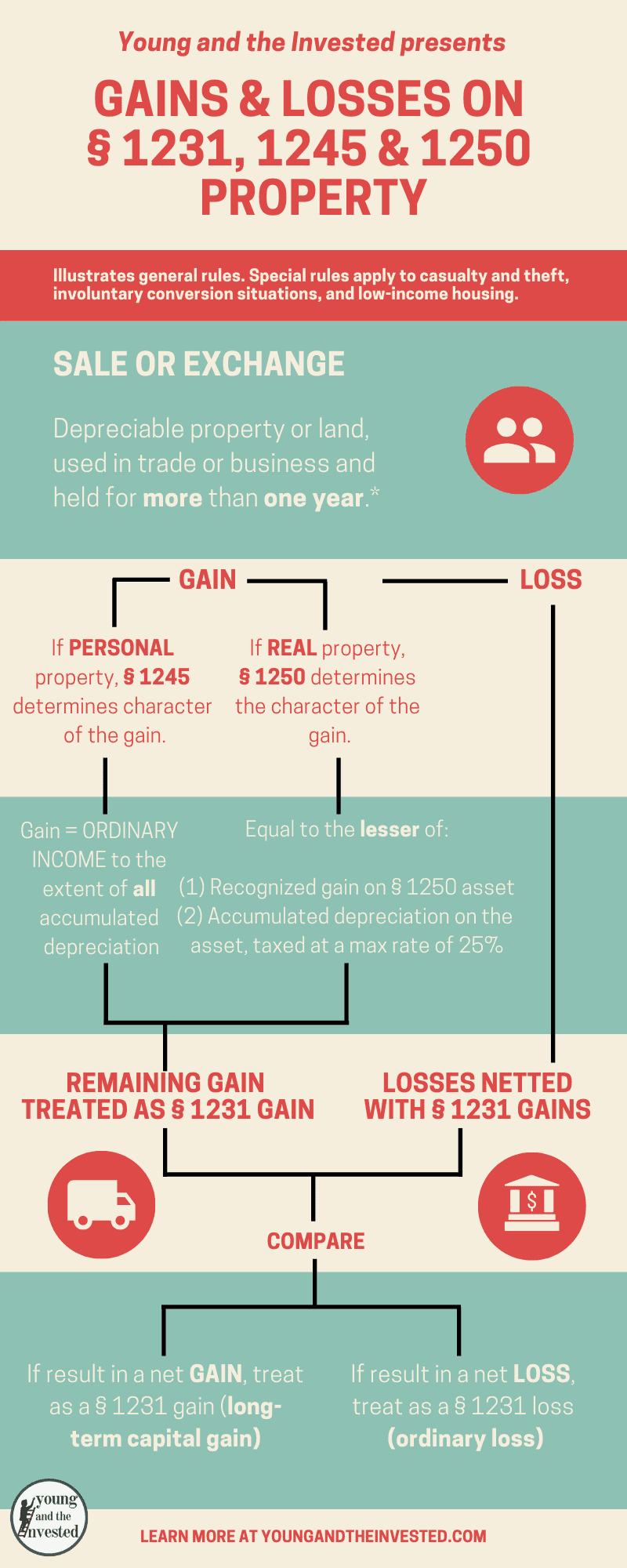

Capital Gains And Losses Sections 1231 1245 And 1250

Like Kind Exchanges Of Real Property Journal Of Accountancy

Depreciation And Income Taxes Asset Depreciation Book Depreciation

Capital Gains And Losses Sections 1231 1245 And 1250

Learn About Depreciation Recapture Spartan Invest